AI is Coming for Banks

Thank you for reading The Sunday Morning Post! Each week I write about the economy, banking, and other topics. To get my articles in your inbox each Sunday morning, just click Subscribe below. Thanks for being here.

Artificial Intelligence has been at the forefront of the business world over the past year with broad existential questions at play about what AI will do to the future of work. AI represents a change that is as significant to the workplace as the computer revolution of the 1980s/90s or the Industrial Revolution of 150+ years prior. The questions before us will test our understanding of human potential as well as the relationship of corporations to their employees not to mention their communities.

AI and the future of work are topics that deserve their own space, and I am sure I will be coming back to them in a future article. For today, however, I wanted to focus on how AI might impact the banking industry and, with it, bank customers and borrowers.

A New Era in Banking

The expansion of AI in the banking world comes at a time when the future of banking is in a state of flux anyway. Younger consumers, who by definition represent the future of the industry, are not as apt to require brick-and-mortar banking locations as has been the typical banking model for the past century and beyond. Younger consumers who were practically born with phones in their pockets and who have since grown up being comfortable with the technology to power online banking not to mention being more lax in their privacy concerns as compared to older generations are just simply not going to go to the traditional teller line to do their banking; they’re doing it on an app. Combine that with the fact that many bank employees such as credit analysts, risk management personnel, and even phone center reps can now do much of their work from home, and it adds up to a world where banks are likely to need significantly less real estate than they have in the past and with potentially fewer employees to boot.

Banks are certain to change significantly in the years ahead. Here are just a few things that come to mind, some of which have been already rolled out in places over the past few years:

Chatbots in lieu of human beings: dozens of industries including many banks have already been implementing automated chat technology to respond to customer concerns in lieu of human beings. These chatbots are prompted to pick up on certain key phrases and terms, and respond according to a calculated algorithm of possible responses. Some of these chatbots are text-based, but others use voice technology to sound like an almost-real human being. Indeed, much of the time the customer is none-the-wiser (although, to be sure, when this technology fails or is clunky, it is a frustrating experience; many businesses have just determined that the cost of those challenges is worth the savings and efficiencies).

Credit analysis: when a bank underwrites a new loan request, it analyzes reams of financial data including tax returns, profit & loss statements, debt schedules, balance sheets, and more. This takes time and labor. Traditionally, of course, this work has been done by actual human beings with deep financial acumen. Credit analysts are commonly people with a CPA-ground or some type of accounting experience and are some of the most important people within a bank. But already today, these documents can be loaded into an AI-portal with a subsequent financial analysis being generated in mere seconds. Granted, there is a lot of nuance in a meaningful credit analysis and the human touch is still necessary, but a lot of the foundational work can and will likely be done by AI sooner rather than later.

Lending: as people may know, I work as a commercial lender. There is certainly a lot of nuance in what we do too, and the best lenders are the ones who know their customers inside and out and can help explain why certain parts of the analysis look the way they do, especially if the numbers are on the line. But I foresee in the future at least some lending decisions being made by algorithmic analysis. Variables such as past payment history with the bank, credit score, the key numbers from a tax return, etc., can be analyzed instantaneously. Some national lenders especially in the FinTech (i.e. Financial Technology) space are already doing this. And to be perfectly honest and reflective about this, sometimes (though not always) lending decisions by algorithm will be actually better than human analysis because the algorithm will not be biased by how much we like the person or are rooting for their success, which can work to the detriment of a clear-eyed look at that borrower’s likelihood of success and propensity to make their loan payments. And for all the benefits of the human touch in flexible underwriting, algorithm-based analysis that can review mountains of data in the blink of an eye will actually be able to identify quantitative issues that the human eye cannot. As banks (and their regulators) assess their internal risk levels, AI-based analysis is likely to reveal things that human calculations might not be able to find.

If you save on capital expenses by not having brick-and-mortar branches for customers and offices for employees, and if you save on personnel costs by not requiring as many credit analysts, lenders, and others, your bank is going to look a lot different in the future than it does today. It is highly plausible, for example, that a chatbot could take an application, a data algorithm could analyze the financials, and the paperwork could be prepared through automation and sent via DocuSign and loan proceeds transferred into a checking account with minimal human intervention.

This is something for current bank leaders including boards of directors and shareholders to think about. Banks employ a lot of people! Those jobs are part of the economic fabric of many communities. If these jobs were to go away, the landscape in many cities and towns across the country from Manhattan, New York to Presque Isle, Maine would look a lot different. And yet the reality of the efficiencies and modernizations that come with technological advances including AI are hard to ignore.

Final Thoughts

The implementation of AI does not need to be doom and gloom, though. History is full of pessimistic takes on new technology that did not prove to be especially cataclysmic and, indeed, made human beings more efficient, more productive, and, in fact, happier in the job. This will happen with AI in many cases. It will also equal the playing field. Noah Smith wrote recently, for example, that AI is likely to boost so-called lower-skill workers, saying:

The machine tools of the industrial age didn’t automate away the jobs of master weavers and smiths; they simply allowed semi-skilled average people to do those jobs just as well as the experts, and at much higher volumes. Replacing high-skilled workers with tech-empowered low-skilled workers is not the same as “automating” work; it’s simply opening it up to the masses.

I think that is a good take. That being said, there are wide swaths of jobs that will be in potential peril in the years ahead. Current workers as well as young people just getting started out should be mindful when making career decisions. In contrast to the previous inflection points in the ways we work, the impacts of the AI revolution are likely to be felt more in white collar settings like banks, accountant offices, and even law firms (although robots building complete houses is not that far-fetched either, so blue collar laborers need to be thinking about this too). I plan to come back to this topic again, so stay tuned for more.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

Addendum: What’s Going on with Nvidia?

Nvidia, which is a technology company at the forefront of AI, has seen its share price (Ticker: NVDA) rise by an astounding 261% in the last year including an increase of 70% just since the start of January. In five years the stock is up more than 2,000%! Nvidia is now the third largest company in the world, trailing only Microsoft and Apple. I don’t claim to have the expertise to properly value a stock as rapidly growing as this one. On the one hand, Nvidia already has first adopter advantages over its competitions. On the other, the trajectory of the NVDA stock price looks a lot like Dot Com stocks of the late 1990s; at a certain point a stock price on a trajectory like this takes on a life of it own, which can lead to both high profits for those riding the momentum train and sudden drops with steep losses (I wrote about this a couple years ago in What Dutch Tulips Teach Us About 21st Century Investing). Anyway, here is the five-year chat for Nvidia:

Weekly Round-Up

Here are a couple of things that caught my eye this week that I thought might interest you too.

Car Dealership Guy on Twitter/X says the cheapest new car right now is the Nissan Versa, which starts at $16,130. But it’s a stick shift.

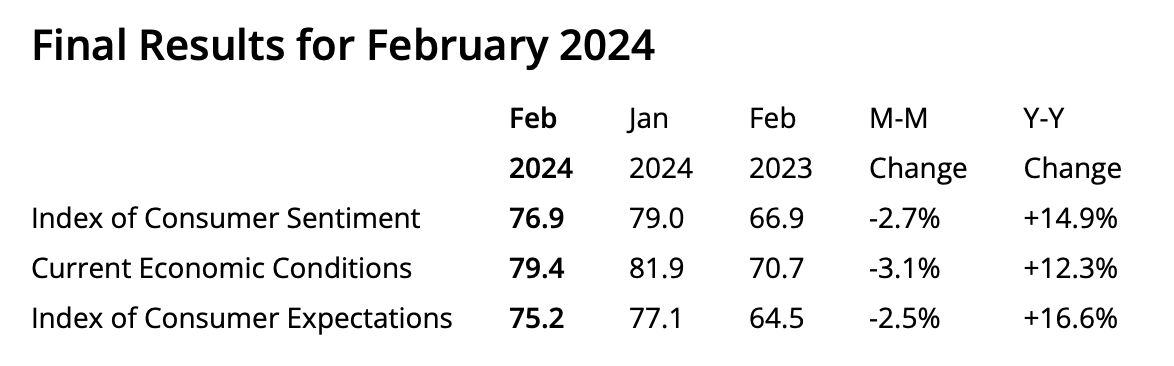

The University of Michigan Consumer Sentiment Report was released this past. week. Sentiment ticked down slightly in February, but is much improved over this time a year ago:

Source: University of Michigan One Good Long Read

Did you know 46 BC is known as “The Year of Confusion?” This article from Martha Henriques of the BBC is chock full of all kinds of history and trivia about the calendar, which is appropriate in that we just had our quadrennial leap day. Apparently the year 46 BC was 445 days long because Julius Caesar added two months to that particular year to catch things up after the previous lunar calendar had fallen behind the solar year, making 46 BC the longest year in history. Who knew?

Have a great week, everybody!