Another No Good, Very Bad Inflation Report

But: is the Fed wrong to keep hiking rates so much, so soon?

The most recent Consumer Price Index monthly report came out this past Tuesday, showing inflation still running hot at 8.3% on a year-over-year basis. Economists had been predicting an 8.1% number, which might not sound like much of a difference, but even a narrow miss can impact the markets and the Dow Jones Industrial Average proceeded to plummet by nearly 1,300 points on Tuesday alone, making it the seventh worst single-day point drop in stock market history. For the week the major U.S. stock market indexes were all down 5.00-7.00%.

What’s Inflating

All categories of spending remain up on a year-over-year basis:

Food (+11.4%)

Energy (+23.8%)

New Vehicles (+10.1%)

Used Vehicles (+7.8%)

Apparel (+5.1%)

Shelter/Housing (+6.2%)

Transportation Services (+11.3%)

Medical Care (+5.6%)

As has been the case all year long, the inflation challenge has been particularly pressing because the increased costs are in the categories most Americans including low and moderate income Americans spend the most of their money: namely food, energy, and housing. That is what has led to particularly hawkish comments from Fed Chairman Jerome Powell lately that the Fed would raise interest rates, inflicting pain in the process, and then keep rates high until inflation is at a more manageable rate of 2.00-3.00%.

Is the Fed Wrong?

I am of the opinion that the Fed got behind the inflation curve by mistakenly reading early inflation numbers in 2021 as “transitory,” which proved to not be the case, and are now trying to overcorrect by inflecting the aforementioned pain and really stamp out inflation. There is a real risk in hiking rates too much, too soon, however, in that it could put a chill on things so fast that the economy contracts more sharply than expected and we enter a deep recession. After recent multiple increases of 0.75% in recent months, the Fed is now considering another 0.75% hike later this month, which some believe could even turn into a 1.00% increase given how hot last week’s inflation report was.

Consider this: although the inflation numbers noted above show notable year-over-year jumps, there is ample evidence that certain things are starting to reverse, like gas, which is down to $3.69/gallon after pushing $5.00/gallon in May, and lumber, which is trading near its lowest levels in recent memory.

Other goods and services are dropping in price too, like used cars, which according to the Manheim Used Vehicle Index are starting to notably decrease after a two-year surge; prices were down 4.0% from July to August alone. Copper and other materials are also down for the year:

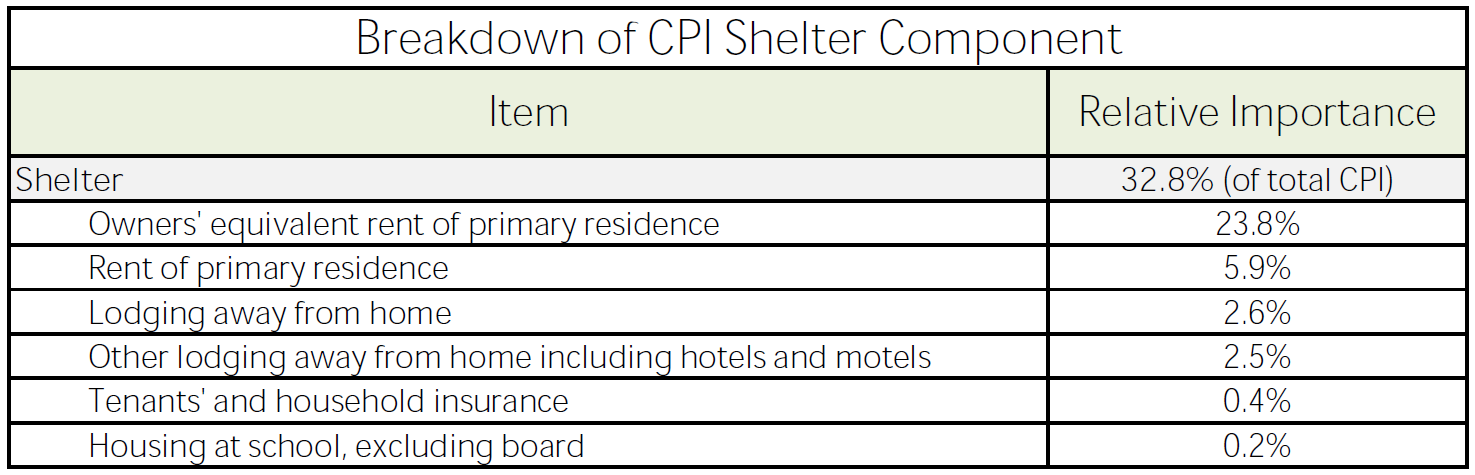

The Effect of Housing on Inflation

Housing/Shelter is a key component of the overall CPI calculations. According to Arbor.com, it represents nearly one-third of the overall inflation statistic:

The problem, however, in using housing data to calculate inflation is that with housing there is generally a data lag. The prices of homes being sold in August, for example, are generally based on Purchase & Sale contracts that were signed in April, May, and June. There is ample evidence that home prices are leveling off, however, and in many markets are dropping. John Burns Real Estate Consulting tracks home prices in 148 U.S. markets; prices are starting to drop in 98 of them. This is unlikely to be reflected in the CPI data until well into the fall, however.

I have been closely following the Phoenix real estate market as it was one of the hottest markets in the country for the past two years. Inflation in Phoenix in the month of August was running at a staggering 13.0%, the largest number for any large U.S. metropolitan market in the last twenty years.

However, not only are home prices starting to drop in Phoenix, but the rental market is decline too. Housing economist Jay Parsons is calling Phoenix “the poster child market for COLLAPSING rent growth.”

If home prices continue to fall and rents also drop in Phoenix as Jay Parsons is seeing them start to do, Phoenix certainly won’t be showing a 13.0% inflation in the months ahead. Now Phoenix is a unique market that has a particularly strong surge in real estate (both homes and rentals) during the pandemic, but if you take this one anecdotal example and multiply it out across the entire country in smaller and less bubbly markets, you can see how the housing/shelter component of the CPI figures may show declines in the months to come, which will drag the entire inflation number down towards more of an equilibrium.

In Summary

Gas is dropping. Lumber and other materials are dropping. Rents and home prices, which, again, represent one third of the CPI statistic, are starting to drop especially in certain markets. Inflation is going to cool, probably as soon as the end of this year and early 2023. If the Fed overreacts by raising rates too much, too soon, the possibility of a soft landing will go out the window and the economy will tip out of balance, sending us into a recession, which means job losses, the stalling of business activity, and fewer purchase of things like homes, vehicles, and vacations not to mention the more pressing expenses of food and utilities. Needless to say, I am not a Fed official, but if I was, I would not overreact in this moment by continue to hike interest rates beyond what the economy and the people in it can bear.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank.