Dumb Luck and Golden Handcuffs

Over the past several decades, there has been a trend of wealth, assets, and income becoming more and more concentrated among a smaller and smaller percentage of the population at the so-called top. According to the Economic Policy Institute, in 2020 the average CEO was paid 351 times the salary of the median worker, a ratio that is up astoundingly from 1965, when the average CEO made a salary of just 21 times the median worker. Meanwhile the top 10% of Americans own 89% of stocks according to 2021 data, and Americans who were invested in the stock market increased their wealth much more significantly during the pandemic than those who did not (although 2022 has been a different story, as the stock market is down over 20% for the year).

Something else happened during the pandemic that will exacerbate this wealth divide for a generation or more to come, and that is the once-in-a-lifetime opportunity that existing homeowners had to refinance their mortgages at rock-bottom interest rates and, similarly, that new homebuyers had to purchase homes at these same low rates while prices were still relatively modest (especially in the earlier days of the pandemic).

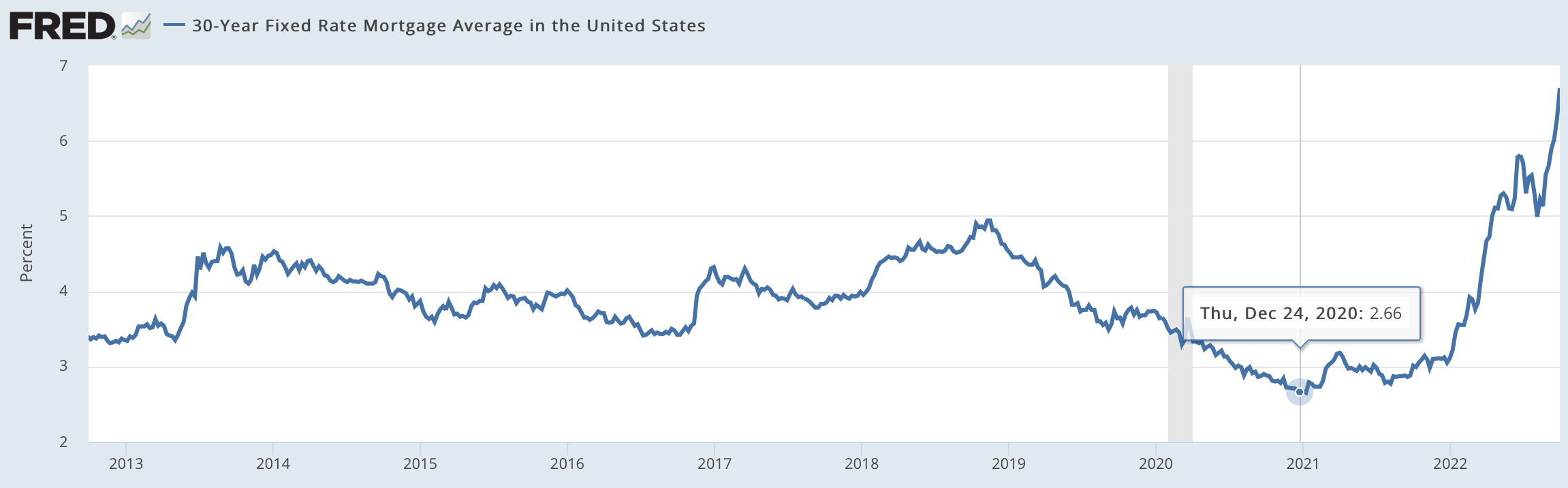

As shown in the chart below from FRED/St. Louis Fed, the average 30-year fixed rate mortgage in the United States bottomed out at 2.66% on December 24th, 2020 - talk about a Christmas present for those who bought or refinanced that month! Rates were well under 4.00% and in the 3.00% neighborhood or below from basically the beginning of 2020 when the pandemic hit, at which point the Fed brought interest rates way down in an effort to boost activity and prevent economic collapse, until the beginning of 2022, when the Fed started raising rates in an effort to cool things off and combat inflation. On December 30, 2021, less than one year ago at the time of this writing, the 30-year fixed rate was still 3.11%. For it to now be pushing 7.00% is really quite a jump in a relatively short period of time.

Here in Maine, the median home price is currently about $350,000. The monthly payment of principal and interest on a $350,000 home at a 3.00% rate is about $1,476. At a rate of 7.00%, that same $1,476/month payment would only be be able to afford a $222,000 home. The average homebuyer in Maine has lost over $125,000 of purchasing power in less than ten months just due to rising interest rates! Nationwide where the median home price is closer to $450,000, the difference is even greater. It is no wonder that the real estate market has slowed considerably in recent weeks.

The Role of Luck

There is a great deal of skill in identifying opportunities based on fortunate circumstances whether you’re a real estate investor or a homeowner. Plenty of savvy investors took advantage of cheap money and scrambled to buy up as many properties as they could over the past few years; one in seven homes purchased by 2021 was bought by an investor, which is not surprising with such cheap money out there. And to be sure, homeowners who were savvy enough to pay attention and financially qualified enough to be able to do so made undoubtedly smart moves by refinancing. So there is some skill/intelligence involved.

But for other people, and I put my wife and I in that category, it was just the dumb luck of fortunate timing that facilitated one of the smartest financial decisions of our lives. We bought our home, where God-willing we will live for the rest of our lives, in July of 2020. The timing could not have been more fortunate. But there wasn't really any skill involved in this. We did not accelerate our plans to take advantage of this narrow window of history, nor were we pouring through reams of data to identify exactly the right moment to buy - it just worked out that way.

It was a blessing, we have always believed, and something that we feel was meant to be, but also really extraordinarily lucky. Had the timing of the circumstances that allowed us to move into our home been slightly different and, for example, if we had been moving in the summer of 2022 versus the summer of 2020, first of all it is unlikely we would have been able to afford the home we live in now, but the mortgage payment would have been many hundreds of dollars a month higher, which is money that we can use instead for other expenses like food, our kids’ activities, travel, saving, and more. This is incredibly lucky, and because we have a July 2020 mortgage instead of a July 2022 mortgage, our financial lives will be forever different.

Inflation Does Not Hit Equally

Housing, including both one’s own home and data from renters, makes up over one-third of the CPI inflation statistic. But for people who locked in 15- or 30-year mortgages from 2020 through early 2022, their housing costs are not inflating. In fact, as I’ve written about before, these Americans have a highly effective hedge against inflation by fixing a huge portion of their costs over an extended period of time. The difference between buying a home in October 2021 vs. October 2022 literally represents tens if not hundreds of thousands of dollars in interest costs over the life of a mortgage, and massive differences to one individual or one family’s budget.

One particularly challenging thing for the Fed to consider today is how to tame inflation and possibly help bring home values back to more of an equilibrium but in a way that does not shoulder current and future buyers with exorbitant interest rates, which will limit their purchasing power and tighten the margins of their budgets. And how does the Fed consider inflation overall as a concept when for millions of Americans their housing costs are actually not inflating, including not just those with low fixed interest rates but those who have paid off their homes and live without a mortgage. Sure, people who have paid off their mortgages still have higher costs at the grocery store and when traveling or buying a new car, but remember, the CPI statistic includes housing as over one third of the calculation. Inflation is not hitting those people the same way right now.

Golden Handcuffs

I thought earlier in the year that as sellers start to feel that the housing market is at a top and has the potential to reverse, which I think we can safely say is exactly where we are right now, that they would flood the market with their homes trying to capture the last gasps of the robust demand we have seen for homes over the past several years. I’m sure some are doing this now, oftentimes listing their homes at crazy high prices just to see if anyone bites.

But what I hear anecdotally from people I am in communication with and with real estate agents I meet with regularly, is that many would-be sellers are simply deciding to stay put. The reason? The costs of financing a new home are simply too great - people don't want to sell a house that has a mortgage with a 3.00% interest rate and buy one with a 7.00% interest rate. This concept is becoming known as the golden handcuffs. Unless you absolutely need to move geographically or you really need to upsize or downsize, the poor interest rate environment is a compelling reason to simply stay put. This limits the available inventory for would-be buyers, further complicating an already bizarre housing market. A healthy market needs inventory, and the much-needed inventory has been sluggish to hit the markets.

Final Thoughts on the Role of Luck

Here in the United States, we value rugged individualism, personal striving, and the relentless quest for a better life. I value all of these things too and, like many Americans, I credit these characteristics in myself for many of my successes in life. But we should also be aware of how much the unpredictable, unknowable, and uncontrollable can factor into our lives too, for better or worse. Being born to the right parents, growing up in a certain neighborhood, whether you had mentors and other more experienced people watching out for you and helping to show the way, and just the infinite other small variables that can tip a person’s life in one direction versus the other: a lot of that is luck, and we should be mindful of its role in our lives and humble towards its benefits or consequences.

The formula for success in life is hard work + fortunate beginnings with an all-American notion that the former in abundance can outweigh a lack of the latter and that anyone can make it in this country, which is a beautiful philosophy woven into the fabric of this very country. But to this formula I would add that most commonly success is the result of hard work + fortunate circumstances + a good deal of luck or at least luck in certain key moments. If you’ve been lucky especially over the past several years, it is worth pausing every once in awhile to count your blessings.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank.