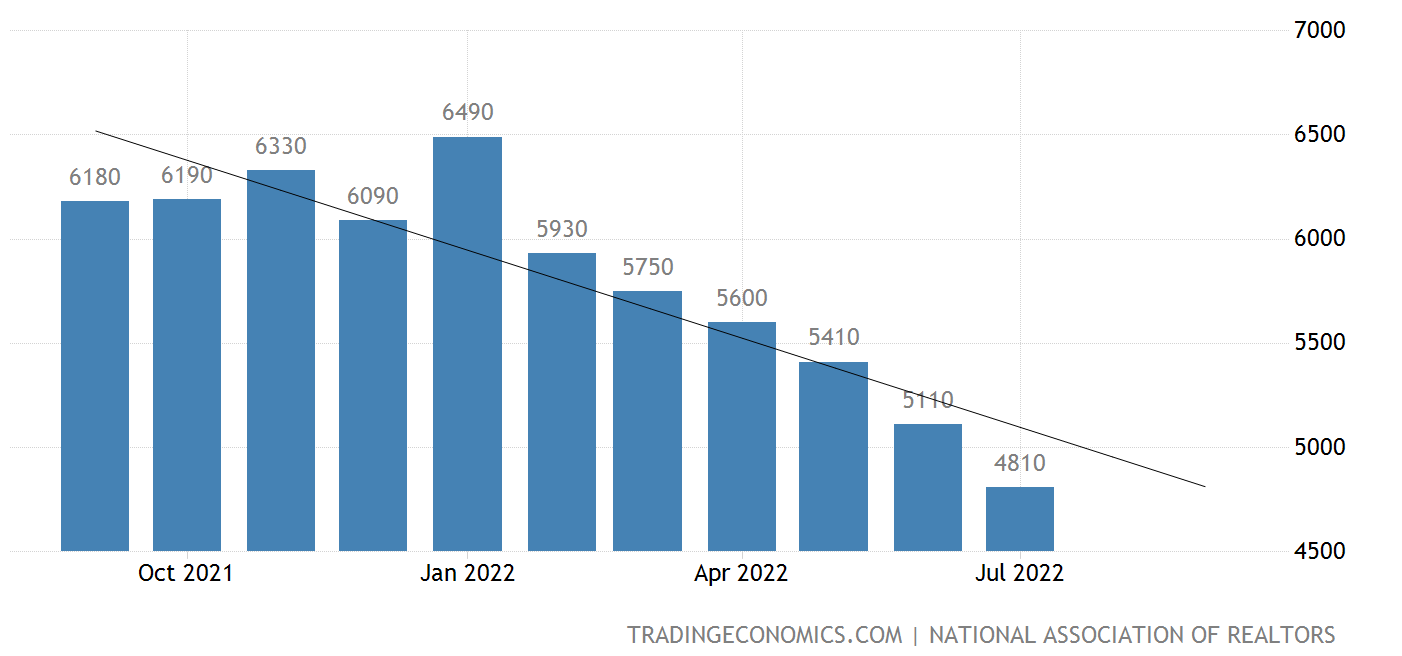

Existing Home Sales Down for Sixth Straight Month

Rising interest rates, low inventory, and an uncertain economy continue to drag the housing market, as the National Association of Realtors released data this week showing that existing home sales have dropped for the sixth straight month:

The 4.81 million homes sold in the month of July were the lowest number since a brief drop in the spring of 2020, immediately following which home sales surged for nearly the next two years. But other than that atypical period of time at the outset of COVID-19, home sales haven’t been this slow since the aftermath of the Great Recession.

It is unlikely that August or September data will show any reversal of this trend once it is available as the challenges the housing market faces are only becoming more significant. As noted on Thursday by Matt Ott in the Washington Post:

Mortgage buyer Freddie Mac reported Thursday that the 30-year rate jumped to 5.89% from 5.66% last week. That’s the highest the long-term rate has been since November of 2008, just after the housing market collapse set off the Great Recession. One year ago, the rate stood at 2.88%.

A one-year jump in the 30-year fixed rate from 2.88% to 5.89% is profound, and many banks are already higher than 5.89% especially for construction loans and non-confirming loans. With the Fed Chair clearly signaling further rate hikes are imminent later this month and in the months to come, interest rates are bound to be even higher by year’s end.

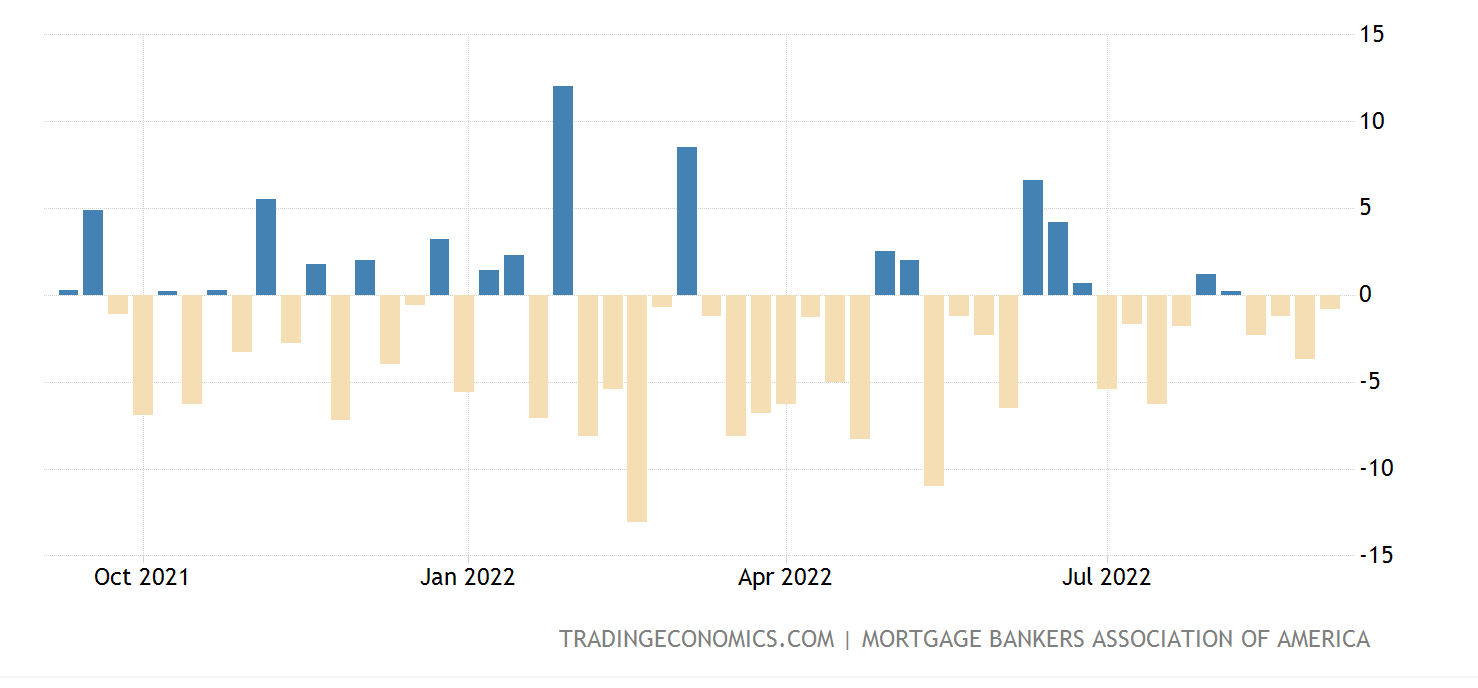

The Mortgage Bankers Association of America reported this week that mortgage applications were down 0.8% over the previous week, the fourth straight weekly decline. The bars below show the percentage change in mortgage applications on a week by week basis for the last year. This past week marked the eighth decline in the last ten weeks, and the 24th weekly decline out of 32 weeks of the year so far.

What About Prices?

Home prices nationwide are still up significantly on year-over-year and quarter-over-quarter bases. According to data from the St. Louis Federal Reserve, the median home sale price in Q2 of 2022 was $440,300, up from $443,100 in Q1 of 2022 and up from $382,600 one year ago in Q2 of 2021. However, keep in mind that homes sales in the second quarter of the year (April, May, and June) are generally based on purchase contracts that were signed in January, February, and March. With that in mind, the transaction prices lag the reality of the market a bit as prices are generally based on market conditions in the 60-90 days prior to closings. I believe that future data will show prices have at least plateaued and, more than likely, are starting to drop by 3-5% nationwide and 10-15% in some of the bubbliest housing markets with perhaps further drops to come in the next 12-24 months.

What to Make of It

If you’re a buyer, patience is key at this point even though rising rates are making it more expensive to borrow. The detrimental hit to buyers through rising rates may be at least partially made up for with more available inventory, less competition among buyers, and lower prices (eventually). I advise patience because buying the wrong house (overpriced, no less) can set a person or family back financially and logistically for years.

If you’re a seller, the power in the buyer-seller dynamic is rapidly shifting from sellers to buyers. So if you are thinking about listing, the sooner the better as by this time next year (or even a few months from now) there are likely to be more sellers than buyers. That is because rising interest rates are going to price-out whole swaths of buyers from the market, and others who do qualify may simply decide to wait for rates to come back down. The housing market frenzy during the pandemic seems to have subsided as homes are staying on the market for longer, price reductions are becoming more common, and there are fewer qualified offers for each listed home.

Lastly, one final note here, if you work in real estate in some capacity, you should prepare for a much different 12-24 months to come (and possibly longer). The volume of transactions has dropped significantly as noted at the outset of this article, and that means fewer commissions for real estate agents, less activity for mortgage brokers and banks, and fewer transactions for attorneys and title companies not to mention fewer contracts for builders and contractors. Nationwide some of the big mortgage companies and other companies involved with real estate like Zillow and Opendoor have already been going through waves of layoffs in recent months. They recognize the writing on the wall: after a frenzied few years, the party is over.

What will the months to come bring? Fewer and fewer sales, especially as we hit the winter, which is always a slow period for the real estate market anyway. In June I wrote that the housing market is changing. Now that we have hit September, it is safe to say that the real estate market has changed.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank.