Hope for Homebuyers

In August, I wrote about how many homebuyers are giving up. The combination of high interest rates, low inventory, and exorbitant prices has been a triple punch that has made purchasing a home simply not viable for many people. Others have backed out of the market of our pure frustration. However, the autumn winds blow leaves of change, and even in the span of several short weeks, there are signs of hope that 2024 will be better for buyers than 2023. Let’s dig in.

Interest Rates

The Federal Reserve provided both relief and clarity this week by announcing it would not raise interest rates in November. The Fed also indicated it may not raise them in December, shifting the conversation from “how many more hikes” to “how long before we can cut.” Markets cheered the news including the stock market, which surged. The yield on the 10-year Treasury Note was a hair over 4.90% to start the week, but it plummeted to 4.58% by Friday, which is a sizable drop in just a few days. The chart below shows the 10-year yield over the past week:

Mortgages rates, which are pretty correlated with treasury rates, also dropped, which is what will be of most interest to would-be homebuyers. The average interest rate on a 30-year fixed mortgage to start the week was 7.92% (it had peaked above 8.00% in October). But by Friday? The average rate was down to 7.38% according to Mortgage News Daily. Mortgage News Daily called it the best improvement in rates in “well over a decade,” saying:

All we know is that this has been some of the best 3 days of news for mortgage rates and bonds that we've seen since rates first began to launch higher 2 years ago. Granted, the magnitude of the drop is greatly facilitated by the fact rates were at multi-decade highs in the past few weeks, but we're not complaining.

The average conventional 30-yr fixed rate is now back below 7.5% for top tier scenarios. You may see a very wide variety of rates today and early next week. This sort of volatility makes lender offerings more stratified than normal. Some of the lenders quoting rates with discount points are already able to do so in the high 6's. Laggards are still near 8%.

How much difference does 7.92% vs. 7.38% interest rate make on a new mortgage? Over $100/month: assuming a $300,000 mortgage, at a 7.92% rate the monthly payment is $2,185/month and at a 7.38% rate the monthly payment is $2,073/month. To be sure, rates are still much higher than they were, say, two or three years ago, but the downward lurch this week provides hope for sure.

Inventory - a complicated picture

Full disclosure, when I set out to write this week’s article I had a belief that inventory was ticking up. In fact, according to data from St. Louis Federal Reserve/FRED, the number of active listings has increased every month since March:

The number of active listings as of September was about 702,000, the greatest it has been since November 2022 and up notably from a low of about 562,000 listings in March. According to data from Realtor.com, the October inventory of homes for sale was 5.1% greater than September, which is notable in that usually inventory declines in October due to reasons of seasonality as people hunker down on major life decisions for the winter.

So what’s not to like here? Well, according to research from Altos Research (and shared on Twitter/X by Mike Simonsen), the increase in inventory is not actually due to more homes being listed; it is due to buyers backing out of the market altogether, which is resulting in fewer sales. In other words, available inventory appears to be ticking up simply because fewer homes are being sold and not because more sellers are actually listing their properties. And as the chart below from Realtor.com shows, yes, you can see in the pink line how interesting it is that inventory is climbing this time of year relative to previous years, but you can also see how much lower the line is on the Y-axis relative to 2017-2019. Whereas there were about 737,000 homes for sale in October 2023, there were nearly 1.3 million homes for sale in October 2017. So we are still way below “normal times” from an inventory standpoint, to the dismay of would-be buyers looking for options.

As I’ve written about before, it will really take a major downward jump in interest rates to loosen up inventory because of the lock-in effect of some many homeowners simply not wanting to move and give up a 3.00% interest rate or better to buy something and finance it at a 7.00-8.00% rate. When everyone stays put, the market essentially is frozen.

Prices

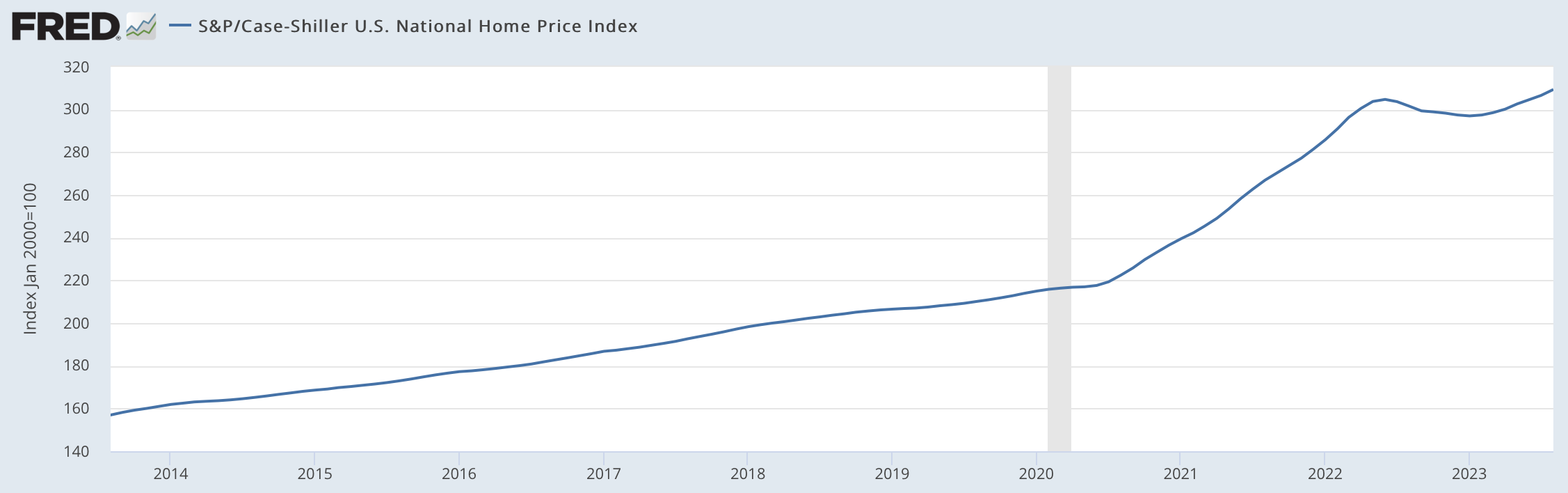

The story of home prices varies a bit by market. Areas of the west and southwest are seeing price drops, while much of the country is still seeing price appreciation including here in the northeast. Time will tell. The Case Shiller Home Price Index showed a drop nationwide in home prices from Summer 2022 to Summer 2023, but price gains have resumed, which certainly is frustrating to buyers.

It is really all about inventory, though. Without an increase in inventory that is a result of more actual homes being listed (as opposed to just fewer buyers in the market), home prices are likely to remain elevated.

What Comes Next

If I were advising a first-time homebuyer today, I would say to be patient. I am very optimistic that the market is going to be much better for buyers in 2024 than it is in 2023. It is likely that interest rates continue to ease down into the spring and summer of next year, which will not only make the math of getting a mortgage more advantageous, but it will also loosen up the inventory. In fact, Wells Fargo is predicting the average 30-year mortgage rate in 2024 will be 6.39% and in 2025 it will be 5.70% (via Lance Lambert on Twitter/X). That will mean thousands of dollars a year of savings for some homebuyers relative to today.

So be patient. Better days for homebuyers are coming. Once the dam breaks on inventory, which, again, I believe will happen once rates come down, prices will ease as a result of all that new supply. Patience is hard especially when you are so eager to make a big life decision like buying a home, but it will get better from here.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

Weekly Round-Up

Here are a few things that caught my eye this week that I thought might interest you too.

Thank you for all the positive feedback about last week’s piece about a mass shooting here in Maine. The New York Times podcast The Daily had a high-quality detailed look this week at all the times over the past year that those close to the gunman including his family tried to get help. Heartbreaking. Listen or read the transcript here.

The 3,840 short-term rental properties on Martha’s Vineyard brought in $4.3 million in local tax revenue in the first quarter of their fiscal year. That is a huge amount. Some states, including here in Maine, do not allow their cities and towns to charge local lodging taxes like this, otherwise municipalities here would earn a lot more local revenue off of these types of properties. Read more via The Vineyard Gazette.

Austin, Texas became the largest city in the country to eliminate minimum parking space requirements for housing developments, homes, and apartment buildings. This is meant to be a way to develop more units, thereby easing the housing crunch (and also to promte public transportation and reduce the impact of cars on the climate). I think it is a good idea. I wrote about this way back in July 2021 here. Read more about Austin via the Texas Tribune.

It is hunting season here in Maine, which provided the opportunity for a pure Maine alert following the 48-hour manhunt for the Lewiston shooter. Via Andrew Mountcastle on Twitter/X:

I had managed to get our family to do a family Halloween costume for the past ten years. Sadly (at least for me), my two oldest children have aged out of this and wanted to do their own costumes this year. I suppose I can’t blame them. But, I’ve still got influence over the littlest:

Have a great week, everybody!

If interest rates stay high, buyers need their incomes to increase at a fast clip to get them back into the house market. Inflation of incomes reduces the burden of high interest rates. However,

it seems that middle- and low-income earners have been missing out for quite some time and there is no great likelihood that this trend will be reversed. People would have to start working hard like the Chinese. Perhaps high-income earners can be persuaded to forgo their next salary increase and their share bonuses and pay more tax to allow the burden of tax on middle and low incomes earners to be reduced? Perhaps Uncle Joe will simply print some helicopter money and the Fed can be persuaded to accept a 5% inflation rate so that the wall of debt faced by the US treasury looks a bit less forbidding and foreigners can be thereby persuaded to lend more so that the volume of imports can be maintained to keep the big box discounters in business?