It's a Good Time to be a Homebuilder

But: rate buydowns becoming more common

These days if you can corral a homebuilder who is not busy on a job site long enough to bend their ear, chances are they are a happy person: overworked and perhaps a little stressed, but happy. According to data from the National Association of Homebuilders (NAHB) and Wells Fargo, homebuilder sentiment has improved for four months in a row. It is also up notably as compared to this time last year. Why?

For starters, demand for new homes just won’t quit. This is fueled by a generally strong economy with rising wages and low unemployment, residential interest rates that are actually down a bit from their highs in the fall of 2023, and, of course, a lack of inventory of existing homes; without many options on the existing home market, would-be homebuyers are hiring builders instead (although as I wrote about last week, the pendulum may be swinging back on this).

The success is being felt by homebuilders big and small. Consider the recent results of some of the largest homebuilders in the country:

DR Horton has seen revenues nearly double in the past five years. Net Income went from $1.6 billion in 2019 to $4.8 billion in 2023. The stock price has tripled in that time.

Toll Brothers similarly saw Net Income more than double from $590 million in 2019 to $1.4 billion last year. The company’s stock price has risen from $37/share to $125/share since 2019.

A smaller though still publicly traded Florida-based company called Dream Finders Homes saw its Net Income go from $39 million in 2019 to nearly $300 million last year.

More homes are getting built and the ones that are getting built are selling for higher prices. Needless to say, this is a good formula for profitability. In fact, not only are gross and net revenues up, but profit margins of virtually all publicly traded homebuilders were notably higher in 2023 than in 2018, as shown in the chart below via Lance Lambert of ResiClub. This means that not only is there more building activity, but it is being done at a more profitable margin:

The Rise of Buydowns

Low existing inventory and a pretty strong economy have provided healthy tailwinds to the homebuilding industry, but builders have another tool in their pocket that is getting deployed more and more often of late: rate buydowns. A rate buydown is a tool sometimes used by buyers themselves to help lower the interest rate on their loan by paying extra at the beginning, thereby saving them money over the life of the loan. But rate buydowns are often being increasingly offered by both homebuilders and sellers (and, especially, when the seller is also the homebuilder!).

According to John Burns Real Estate Consulting, as of last fall, a full 60% of homebuilders were offering buyers rate buydown options as an extra incentive to buy. The mechanism to do this is often as simple as the builder contributing funds directly to the buyer’s financial institution to help buy down the rate, but many builders themselves also have their own mortgage financing options, oftentimes from closely partnering with a home financing company or bank. The fact that both prices and profit margins (as noted above) have gone up so much means that homebuilders and sellers can sometimes offer a rate buydown as much as 10-15% of the purchase price and still make it a profitable venture. Homebuilders that are operating at maximum efficiency (and maximum profit) can even offer rate buydowns purely as a competitive advantage to box out other builders who may be less inclined or less able to offer such attractive incentives.

How Long Will the Builder Boom Last?

This past Friday, the latest jobs report showed an additional 303,000 jobs were added to the economy, which helped drop unemployment to 3.8%. Wage growth on a year-over-year basis was 4.1%. As long as the labor market holds up like this, homebuilders should still see plenty of activity. Of course, eventually the economy will falter and homebuilding activity will decline as people are less inclined (or less financially able) to make major life decisions like building a new home in a down economy.

The other variable is existing inventory, which I wrote about just last week so I won’t dwell on it here other than to reiterate that if interest rates do drop at some point, which eventually they will, it could lead to a breaking of that inventory dam and many of the sales that were meant to have happened but didn’t due to the lock-in effect will start to gush forth. Once the existing inventory of homes for sale rises, it could take some of the frothiness out of the new-home construction market as buyers will have more choices.

There are other important variables too, like the cost of building materials and the supply of construction labor, which in some places like here in the Northeast is a major challenge as there are just not enough workers. I spoke to one homebuilder this week who said he “could build 20 more houses this year if he just had the crews.”

Lastly, and a bit beyond the scope of today’s article but still worth mentioning, eventually AI is coming for many different jobs and industries, including, in my opinion, homebuilders and the construction trades. It it not out of the realm of possibly that in the intermediate-term future and beyond, homes will be built by computers, robots, and other AI-tools. In fact, it is already starting to happen. I could envision as soon as 10 to 15 years from now actual human homebuilders differentiating themselves from companies that are building with the use of robots by marketing “hand-crafted homes.” Competition from AI could very well be bad news for builders in the years ahead, although potentially positive for buyers if it helps to lower costs and increase timelines. Time will tell.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

A Brief Weekly Round Up!

Along with millions of Americans in a swath of states from Texas to Maine, we are about to experience Monday’s total solar eclipse. My hometown of Bangor, Maine is just outside of the path of totality, but only just barely so. Schools are letting kids out at noon (and some schools that are fully in the path of totality have no school at all). We are planning to drive north 30-40 miles to experience it. Once in a lifetime!

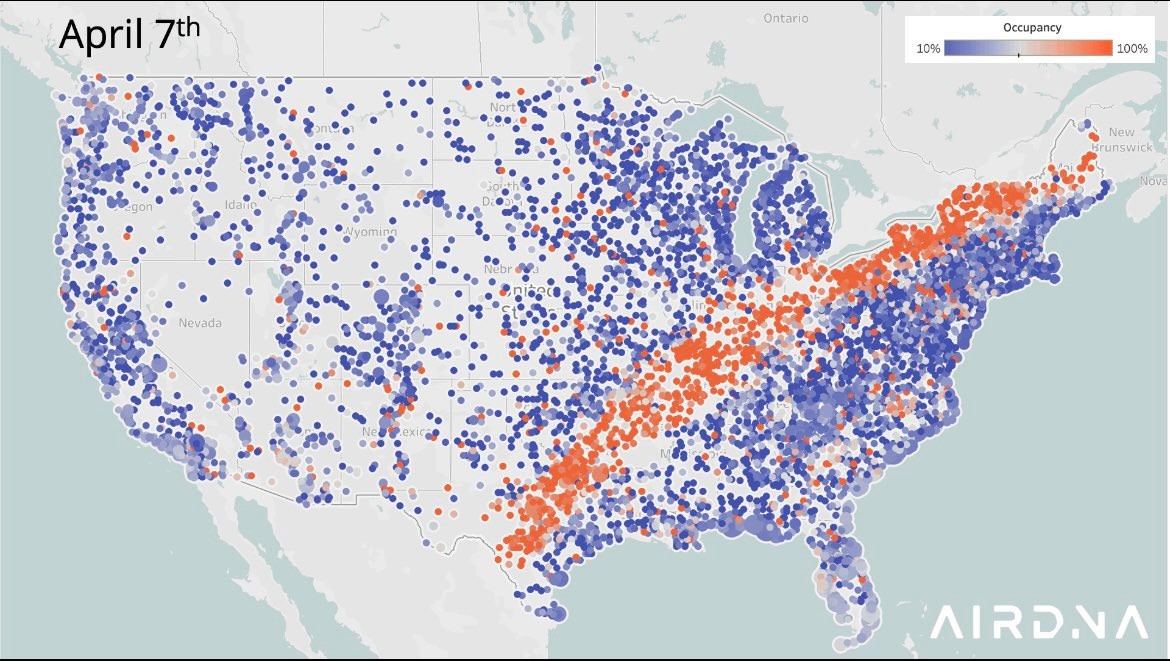

Curious about what the actual path of the eclipse is? Just check the map of where AirBNBs are fully rented on the night before the eclipse (via Jamie Lane of AirDNA). Fascinating stuff.

I’ll be back with more Weekly Round-Up links and One Good Long Read next week. This past week has been busy with work and family. Have a great week, everybody!

I remain flummoxed that this data and much more does not seem to be moving the needle re the Presidential race.

Almost impossible to build at scale here Maine. Labor is a huge part, but so is lack of suitable land and zoning, entitlement issues, lack of infrastructure (I.e sanitary sewer) and NIMBYISM. And then banks willing to underwrite home building projects at scale.