Rental Market Preview 2023

Hope for tenants; caution for investors.

The past few years have been quite positive for rental property owners, who have seen their real estate values rise along with higher income from increasing rents. Vacancies have been at historically low levels and the cost of borrowing has been cheap, at least up until about six months ago.

That’s not to say that being a real estate investor is easy or that the income is “passive.” Supply chain issues, rising utility costs, higher costs for repairs and other capital expenditures, plus navigating COVID-19 have made it a challenging time in many ways. But in general, I think it is safe to say that it has been a good time to be a real estate investor.

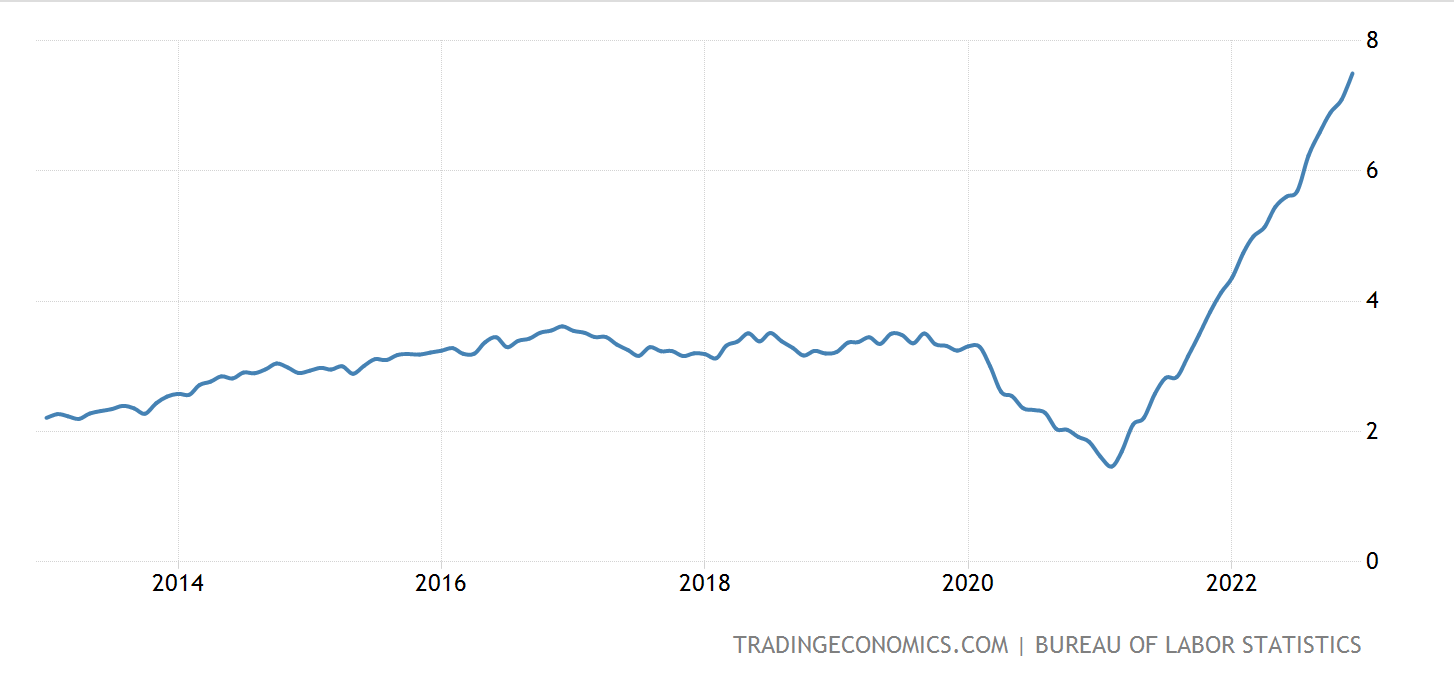

Rent inflation was up 7.5% in 2022, a high figure not seen since 1982. In fact rents have been sharply rising ever since a temporary downturn in the early days of COVID. The line graph below via the Y-Axis on the right side of the chart shows the annualized percentage growth in rents over the last ten years:

What Comes Next

Last week I wrote about what might happen to the housing market over the next year. Many of those same conclusions are applicable to the rental market as well. I believe real estate values for both homes and rental properties will modestly decline this year, which will be attributable mostly to high interest rates pushing buyers to the sidelines. In certain markets (though not necessarily the Northeast, from where I write), the declines could be substantial.

If the market for homes has frozen up a bit over the past few months, all the more so with residential rentals. The cash flow for an investor who is financing their acquisitions just does not work as well at an 8.00% interest rate versus a 4.50% interest rate and so deals are not as viable. Fewer rental properties will be transacted in the months ahead as purchase activity continues to dampen due to these ongoing higher rates, which the Fed has signaled are unlikely to come down for at least the next 8-12 months.

There are some other pieces of data and variables at play in the rental market that are worth analyzing as we look ahead. And that is the purpose of today’s article.

Just as an editor’s note, I generally write to an audience that is comprised of many real estate investors. I try not to make value judgements. Sometimes what is good for investors is not as positive for tenants, and vice versa. What I seek to do is lay out the data, use my perspective to analyze it, and let you come to your own conclusions. What is positive or negative will depend a lot on where you sit in the rental ecosystem.

Vacancy Rates

The rental vacancy rate in the third quarter of 2022, which is the most recent quarter for which data is available, was 6.0%. This was up modestly from a 5.6% vacancy rate the quarter prior, but these are historically low figures. The last time the vacancy rate was this low was the second quarter of 1984.

The chart below shows the steady decline in vacancy rates over the past decade:

Why are vacancy rates so low? I wrote about this in May and would refer you to that article for more discussion. But in summary, there are a variety of reasons including a period of under-building from 2008-2011, which has rippled forth to this day in the form of lower inventory. Home prices have risen considerably since the early days of the pandemic, which has pushed would-be buyers to the sidelines and consigned them to be renters instead. And a good amount of rental inventory has been converted to short-term rentals like AirBNBs, which has contracted the rental market to fewer available units.

But what comes next? I believe it is likely that vacancy rates will rise modestly this year. It would not be surprising to see vacancy rates closer to 7.50-8.00% by the end of 2023.

New Inventory

We still do have a housing shortage, there is no doubt about it. Bank of America puts the gap at 4 million homes. But there are also massive waves of new rental inventory coming online in the months ahead, primarily through two sources: new construction and the conversation of other properties into residential rentals.

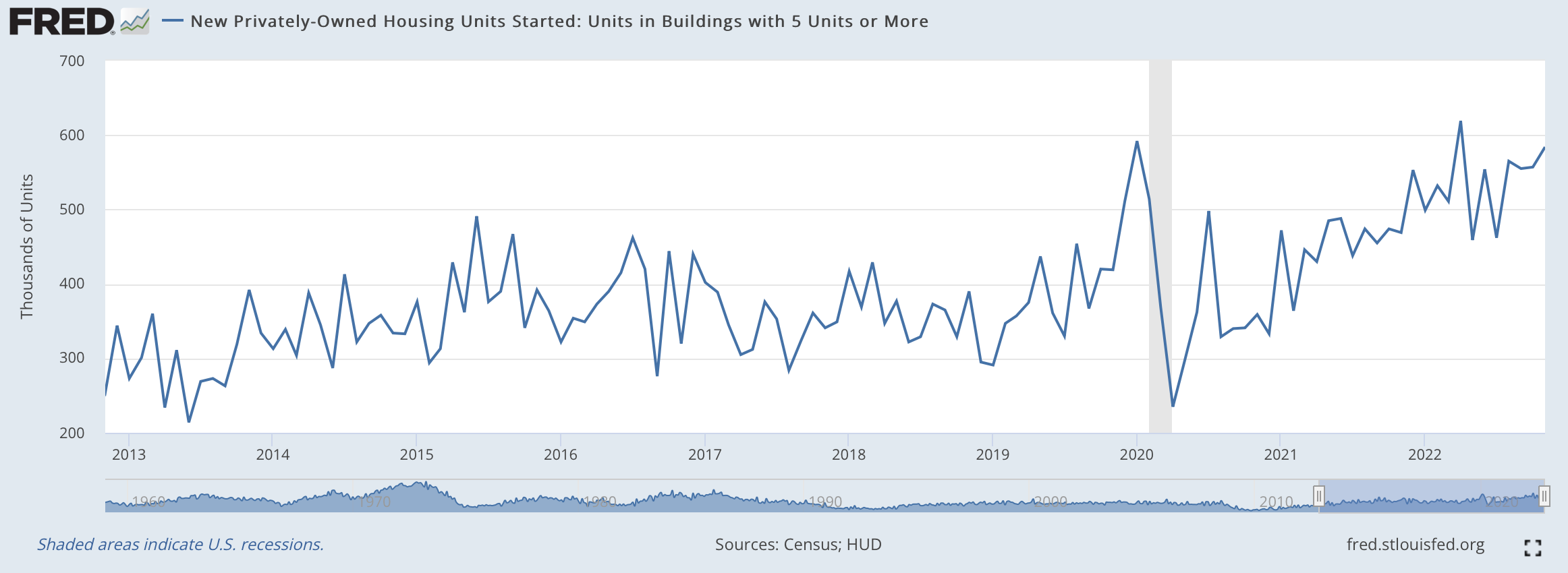

Consider the chart below showing multiunit rental property starts over the last ten years. The trend is clear: there are a lot of new rental properties being built. And as these new units come online, it will provide renters with more options, thereby spreading out the pool of available tenants.

There are definitely some headwinds that could ease down this rate of construction. The same high cost of borrowing faced by homebuyers and real estate investors is hitting builders as well. While some of the supply chain issues have settled out, we still have a very tight labor market, which makes the building process slower and more frustrating. On the other hand, material costs are down. And anecdotally speaking, I am hearing from developers that cities and towns are more amenable to new residential construction these days because local policymakers have heard from constituents loud and clear that they want action on fixing the housing crunch. Projects that might have been held up by red tape and NIMBY-ism a few years ago are grinding their way through the permitting and approval process somewhat more easily today (although, to be sure, NIMBY-ish remains a powerful force counteracting hopes for new development).

The other source of new rental inventory is the conversion of non-rental properties into rentals. For example, with a weak sellers’ market, there is evidence that would-be home sellers are holding onto their properties in order to rent them out instead. I have seen this a few times with homebuyers who are opting to hold onto the home they are leaving in order to earn rental income from it (and to keep the 3.00% or better interest rate on that asset). John Burns Real Estate Consultants has data showing that 9% of sellers have switched their listings to be rentals instead, up from 4% in July. In certain areas of the country including the southwest, which of course includes bubbly real estate markets like Phoenix and Las Vegas, a whopping 17% of home listings have been changed to rentals.

Other new inventory is coming in the form of office buildings and other properties being converted into residential. This is a topic I plan to come back to in a future article, but suffice it is to say that these types of conversions make financial sense in a world where more workers are working remotely or from home, thereby decreasing the need for office space, and while there is such strong residential demand.

What all of this new inventory will do is, simply put, provide tenants with more available options. Yes, many renters are priced out of the market to buy a new home and so they will have to continue to rent instead, but with much more rental inventory coming onto the market in the months and years ahead, some pressure on tenants will subside. Quite positively, many of these office buildings are in the urban core of cities. Adding more people living to these areas can increase vibrancy and spark further mixed-use development.

Life Decisions and Adjustments

The other major factor at play in the current rental market is that as the economy changes, people make adjustments in their lives. Although the labor market remains strong, there is a general feeling that the economy is tipping towards recession. And that makes people understandably nervous. When people are feeling uncertain economically, they change their behavior. How does that look in the rental market? For starters, adjustments that people are already making include living with more people to share rent costs together or moving back in with family, both of which contract the pool of tenants overall. Combine this tenant pool contraction with all of the variables noted above regarding the creation of new inventory, and it is a formula for a softer rental market and rising vacancy rates.

Consider, too, the chart below showing the average number of people per household going back to 1960. The major driving force here is the declining birth rate; families just aren’t as large as they were generations ago. But, if we do have a down economic period, I would expect that historically low number of 2.5 people per household to tick up slightly. And this is a piece of data where even hundredths of a percentage point make a huge difference nationwide. You can see below how the number of people per household increased from 2.56 to 2.59 during the Great Recession from 2007-2010. The rental vacancy rate during that same time period? It went from 9.5% in the second quarter of 2007 to 11.1% by the third quarter of 2009 before beginning its steady, decade-long decline. Down economic periods typically make vacancy rates go up as demand for rentals softens.

Changing Yields

Another variable impacting the rental market is that the yields on other investments have risen considerably in the last year. Yields on 10-year Treasury Bills are around 3.50% and were above 4.00% for much of the fall. A year ago they were under 2.00%, so investors can really get a better rate of return today than they could last year. Yields on other types of bonds including corporate and municipal bonds and rates on CDs and other safe investments have also risen. As these yields continue to rise, some real estate investors may ask if all the work of tenant management and property maintenance is worth it when there are other investment options out there that would be truly passive. Some investors may shift assets to paper investments instead of hard assets including real estate.

The Overarching Variable

What other variable will most significantly impact the rental market in 2023? As James Carville famously said in 1992, it’s the economy stupid. I believe the Federal Reserve is at risk of raising interest rates too much, too fast in order to tame inflation that is already coming down. This week’s inflation report showed further cooling, which will only become more pronounced in future reports as delayed data for home sales and rents starts to get baked into the analysis. If the Fed does drag the economy into a recession and people start to get laid off, many will struggle to pay their rents. It is unlikely there will be much help coming from Washington D.C. as there is a general fatigue towards more stimulus funds after several rounds of COVID-relief during the pandemic. And now with a split government with the Republicans holding a narrow advantage in the House of Representatives but Democrats in control of the White House and the Senate, it is pretty unlikely there will be any meaningful legislation that would offer rent relief both because the Republicans wouldn’t support it and not much legislation will get through the gridlock anyway.

Over a year ago in October 2021 I wrote about the likelihood of closing the housing supply gap. At the end of the piece, I tagged on a word of caution for rental property owners about the potential for a perfect storm to hit margins and undermine profitability:

So file this away in the back of your heads, all you readers who are also rental property owners: the nightmare scenario for property owners is that in 5-7 years interest rates have risen so the cost of borrowing is higher, the economy is in a trough so tenants are in financial peril themselves and are having trouble making their rent payments, which could also lead to the reversal of rent inflation, and there are millions of new housing units that have been built and hundreds of thousands of more landlords and property owners offering potential places to live. The rental market might not be quite so hot (or profitable) for property owners in such a landscape.

The only thing I would change about that word of caution today is that a good portion of this is happening right now over a 2-3 year timeframe instead of 5-7 years.

A Final Word

So will rents come down in 2023? I think in many markets they will. Indeed, there is already evidence that they are. At the outset of the article I shared a chart showing rent inflation was 7.5% in 2023, but this data does lag for a variety of reasons and the reality at the current time reflects differently than what the CPI data might show. There is evidence now that rents are already starting to come down. Emily Peck had reporting in Axios in October arguing that the CPI data on rents was misleading and showing that rents were down 2.5% in September on a year-over-year basis. And as Matty Yglesias of Slow Boring notes below, data from current rent listings shows a rapid deceleration of rising rents (a fancy way of saying rents are easing up).

I do not think we are necessarily in for a real estate crash in the rental market. The housing gap is just too wide and as long as it remains so expensive to buy a home there will be millions of Americans who will have no choice but to rent instead. Millions of Americans are of course renters by choice, too, including a large number of high net-worth Americans who do not want to be anchored to a home or to one geographic area for too long.

But the headwinds are there. I believe that just as the power dynamic has shifted from buyers to seller in the home market, so too will much of the power shift from property owners to tenants over the next couple of years. I do not think this will play out as rapid property devaluation or a complete crashing of the market, but rather a significant tightening of margins and more challenges maintaining tenants as they are likely to have more options and to enjoy a more competitive rental landscape. This, of course, spells good news for tenants, but residential real estate investors should continue to test their assumptions, challenge their models, and diversify their assets as the market does continue to change.

Ben Sprague lives and works in Bangor, Maine as a Senior Vice President/Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank. © Ben Sprague 2023.

Ben, I'm older and simplified but have friends still in real estate. I read your posts and have recommended them many times. Good work.

Good information as usual. An interesting topic for the future may be the true cost of renting to low income people, particularly for newer investors. I hear so many who think their money is guaranteed like section 8 but have no idea of the reality. Now many have received stimulus assistance which can also be a red flag for the property owner. My son recently gave it a try renting to low income and it cost him 30% of his annual income so far, lesson learned.