The Return of the Variable Rate Mortgage

From March 2020 to December 2021, American homeowners were generally able to obtain new mortgages or refinance existing mortgages at rates around 3.00% or below. New commercial loans and commercial refinances were similarly low, although commercial rates tend to be higher than residential rates, generally speaking.

These were historically unprecedented low rates. In fact, interest rates on home mortgages have never been lower in the history of banking in the United States than they were during the throes of the COVID-19 pandemic, which ended up being a real silver lining of the whole grueling period because the lower cost of borrowing helped to not only boost the housing market but also had ripple effects through the entire economy. With less money going towards their monthly mortgage payments, homeowners had more money to spend on other things like home renovation projects, entertainment, travel, and shopping (to the extent that these things were even possible during much of the pandemic).

But now interest rates have spiked. The average rates on a 30-year fixed mortgage was 3.11% on December 30th; it is now above 5.00%. Rates on non-conforming mortgages and construction loans are even higher and are frequently pushing 6.00%. These types of loans have been especially popular of late as there is just not enough existing inventory of existing-homes-for-sale so many would-be homebuyers are opting instead to build.

As fixed rates rise, an old bogeyman is back on the block: the variable rate mortgage, or 5/1 ARM (in which the initial interest rate is generally lower but only fixed for five years and then becomes variable).

Variable rate mortgages tend to get a bad rap for a couple of reasons. First, there are plenty of predatory lenders out there who lure consumers in with the promise of low rates without adequately explaining the variable component. Once rates rise, which they are doing now, these mortgages become more expensive and the payments can become challenging for borrowers, leading to potential defaults and foreclosures. This type of predatory lending is unequivocally bad. Some of it has been partially reigned in by new banking regulations following the Great Recession, but there will always be bad actors out there who will take advantage of uninformed but trusting customers.

The Great Recession itself is, of course, the other reason why many people tense up at the mere phrase variable rate mortgage, and that is because these types of mortgages are largely considered to be a key catalyst for the economic collapse we saw in 2008. As the conventional wisdom goes, borrowers took out ARM’s that were attractive when they first obtained them, but then rates went up and the monthly payment amounts increased, which lead some homeowners to default, sending the housing market and the economy as a whole into a tailspin.

This conventional wisdom is only partly true. For sure, defaults on variable rate mortgages were a key catalyst for the chaos we saw in 2008. But it was really the big banks’ collateralization of these mortgages into leveraged debt instruments that was the real problem. Once a portion of these mortgages started going into default, the leveraged debt that had been pieced together and sold by the big banks became what famed investor Warren Buffett called “financial weapons of mass destruction” that threatened to bring down the entire economy.

I would submit that the variable rate mortgage itself, though often sold under faulty pretenses or without full disclosures of the risks, was many times less dangerous to the economy than the highly leveraged risky bets that Wall Street and the various megabanks were making on the housing market at the time.

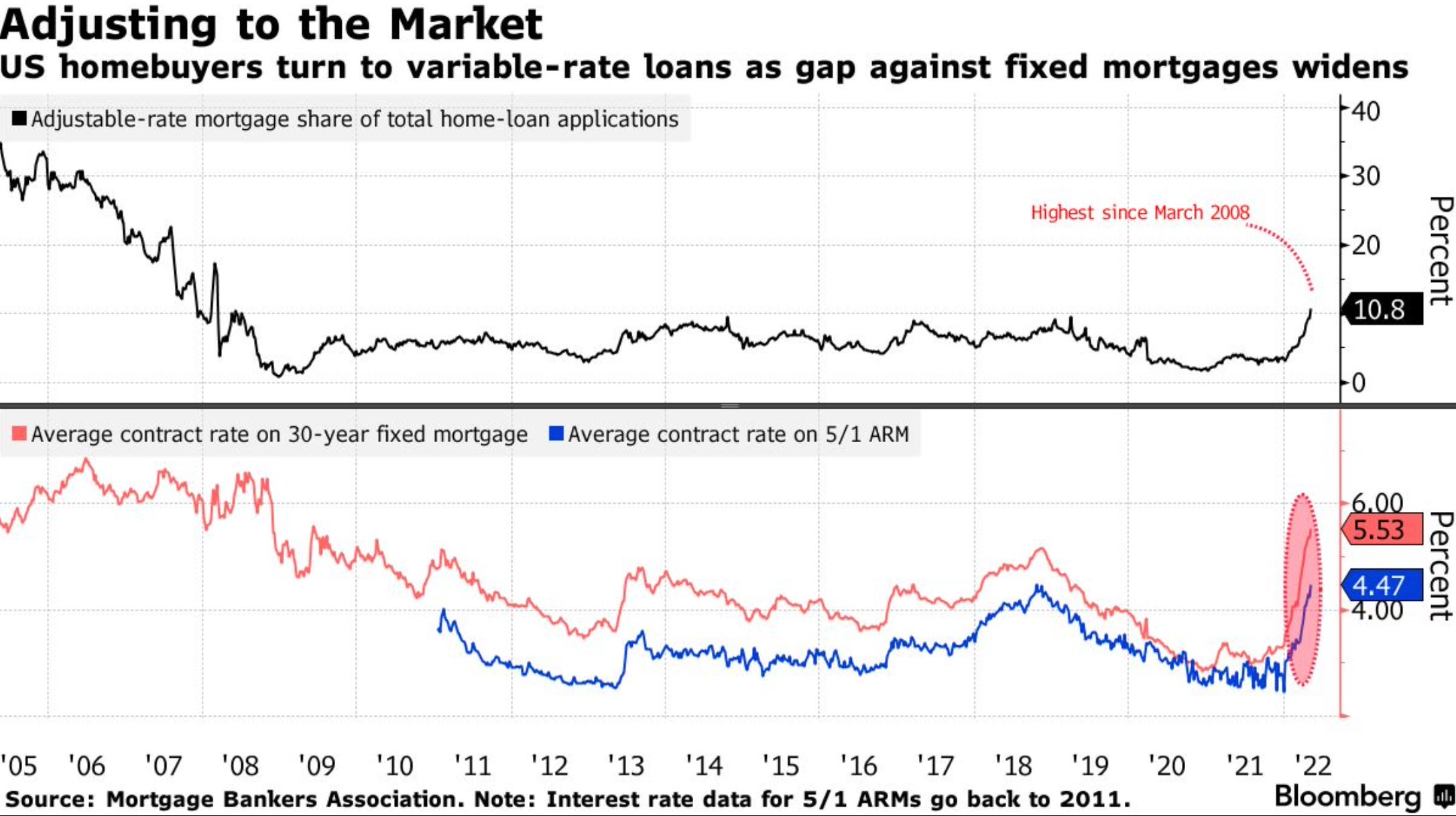

And now, the variable rate mortgage is coming back. Per Bloomberg, at the start of the year, only 3.1% of mortgage applications nationwide were for a variable rate. This statistic makes sense as fixed rates were so low at the time that it really didn’t make sense for people to opt into a variable rate. But as of the first week of May, the percentage share of U.S. mortgage applications that were variable had increased to 10.8%, which is the highest percentage since 2008 (prior to 2008, i.e. the lead-up to the Great Recession, the percentage share was even higher, as illustrated in the chart below):

Why are ARMs becoming more popular? For a simple reason: price-conscious consumers are looking to save wherever they can. As shown in the chart above, the percentage savings up-front of a variable rate versus a 30-year fixed rate is about 1.0%, which can represent thousands of dollars over the course of a year and tens of thousands over the life of a mortgage. The risk, of course, is that after five years the rate is no longer 4.47% as illustrated above, but is more like 7.47%, which would jack up the payments for millions of American homeowners who may not actually be able to afford them especially if the economy hits a rough patch.

Where are interest rates going, one might ask. In the short-term, almost certainly up. The Fed has signaled another rate increase of 0.50% at its next meeting followed by either another increase of 0.50% or smaller increases of 0.25% throughout the rest of the year. But then what about one, three, five, or even ten years from now? It is harder to forecast. My take is that inflation will cool down over the next 12-18 months. Plus high gas prices and generally high costs for everything (i.e. inflation) will itself help reverse things as consumers will pull back from discretionary spending. I wrote in early April about how there were already signs that we were hitting peak inflation with a potential deceleration of inflation to come. With this in mind, my hope is that the Fed does not overshoot on raising interest rates and, perhaps, after a series of immediate hikes that are expected over the coming months, rates will either plateau or possibly reverse and start to drop.

The increase in variable rate mortgage applications presents a lot of risk to the individual consumer and to the economy as a whole if interest rates rise at an uncontrollable rate and for an extended period of time. That enough is reason for both banks and consumers to be cautious: banks in their underwriting and consumers in their choices. Banks can, should, and do underwrite potential borrowers not only based on current interest rates, but also based on their expectations of future rates. It is entirely conceivable that a borrower would qualify for a loan (commercial, residential, or otherwise) based on current rates, but not based on a shock of 200 basis points (2.00%), in which case the bank will often decline the loan.

Given how high home values have risen and the amount that can be saved by shaving off a percentage point as compared to a fixed rate, the share of variable rate mortgages is only likely to increase. With that being said, there is also a school of thought that hypothesizes that rates will increase for the next two years and then actually retreat again in the face of economic headwinds, which, ironically may be brought along by rising interest rates themselves. For all the upside risks of a loan with a variable rate, borrowers actually win by having a variable rate if rates were to decline. Whether the upside risks are worth it in a rising interest rate environment, however, is up for each person to decide.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank.