The Worsening Vibes

Greetings, Sunday Morning Post readers! A couple of quick notes to start this week:

I am experimenting with Substack’s chat feature, which is meant to give us a way to stay better connected and to talk together as a community. You can find it here. Join in!

I am preparing a presidential election preview (Biden vs. Trump - have you heard of them?) for Memorial Day Weekend, because who doesn’t want to think about that on their long weekend? Today’s article is a bit or a precursor to that: a look at the collective views on the economy by the American electorate.

As a quick reminder, there is now a paid subscriber option for The Sunday Morning Post, which you can read about here. Offering a paid subscription is a way to make sure the newsletter is sustainable and can expand.

Americans are feeling increasingly sour about the economy. This has to be frustrating to the president and his allies as he presides over an economy with an unemployment rate below 4.0%, rising wages, and a stock market that is up more than 10% for the year and up more than 25% in the last 12 months. I’ll have more thoughts on the presidential horserace next week, so stay tuned for that. For today, I thought it would be worth doing a dive into why Americans are frustrated and what the trends and data suggest about the economic cycle that lays before us.

I wrote this past Thanksgiving about how the vibes are off in this economy. We are now well-past the quarter-pole in 2024, and it does, in fact, seem like those vibes are worsening. Recent Gallup polling shows just 24% of Americans rate the economy positively, while 76% have a more dour view, saying the economy is “only fair” or “poor.” Moreover, 67% of Americans say that economic conditions are getting worse, a tick up from 63% in March and 61% in February. Just 29% say the economy is getting better. These are pretty decisive numbers, and reflect an unsettled American electorate.

The biggest driver of the negative feelings out there has been the same for the past three years: inflation, or the high cost of living. Although inflation has decelerated substantially from its 2022 peak, when year-over-year inflation topped out at over 9.0%, it has not subsided as much as the Fed would like to see or, just as importantly, to a level that makes American consumers feel comfortable and happy.

Indeed, consumer sentiment, which had been fairly buoyant for much of the past year despite the prevailing inflation, has dropped in the last month. Earnings calls these days from company CEOs are filled with anecdotes about people pulling back from big ticket items. Per the most University of Michigan consumer sentiment survey:

Consumer sentiment retreated about 13% this May following three consecutive months of very little change. This 10 index-point decline is statistically significant and brings sentiment to its lowest reading in about six months. This month’s trend in sentiment is characterized by a broad consensus across consumers, with decreases across age, income, and education groups. Consumers in western states exhibited a particularly steep drop. While consumers had been reserving judgment for the past few months, they now perceive negative developments on a number of dimensions. They expressed worries that inflation, unemployment and interest rates may all be moving in an unfavorable direction in the year ahead.

Inflation persists. Per the latest CPI Report for April, which was released just this past week, year-over-year inflation came in at 3.4%, which, again, is much better than the 9.1% peak in June 2022, but it is still too high. Indeed, for the entire past year, inflation has been in this 3.0-3.7% range the entire time, struggling to crack below that 3.0% barrier or beyond.

More specifically for American consumers, some of the biggest drivers of inflation have been in the categories of spending that people have little control over including shelter and food. After some much-needed relief in energy prices over the past several months, April saw a notable tick up in gasoline and electricity costs (although heating oil prices did drop). People are feeling this in their personal and household budgets, and the consternation is evident in the polling.

A Closer Look at Debt

Something unique happened during the pandemic, which was that Americans’ collective debt levels fell. This was highly unusual, as debt has, in general, steadily expanded over the course of time. The drop was attributable largely to two things. First, with the entire economy mostly shut down for a period of weeks or months depending on where you live and how restrictive the rules were, people spent less money on things like eating out, traveling, entertainment, and other discretionary activities. Some of this spending was temporarily diverted into paying down debt instead as people suddenly had extra surplus funds. And secondly, fiscal stimulus programs like direct checks to Americans and massive business relief programs like the PPP loans injected quite a bit of additional money into the economy, some of which went to paying off loans and credit cards.

But several years later as people try to make ends meet amid rising costs, debt is on the upswing. Consider the following:

Credit card balances have topped $1 trillion for the first time ever (by the way, check out the trough in the chart below of collective credit card debt corresponding exactly with the pandemic; what a beautiful chart!):

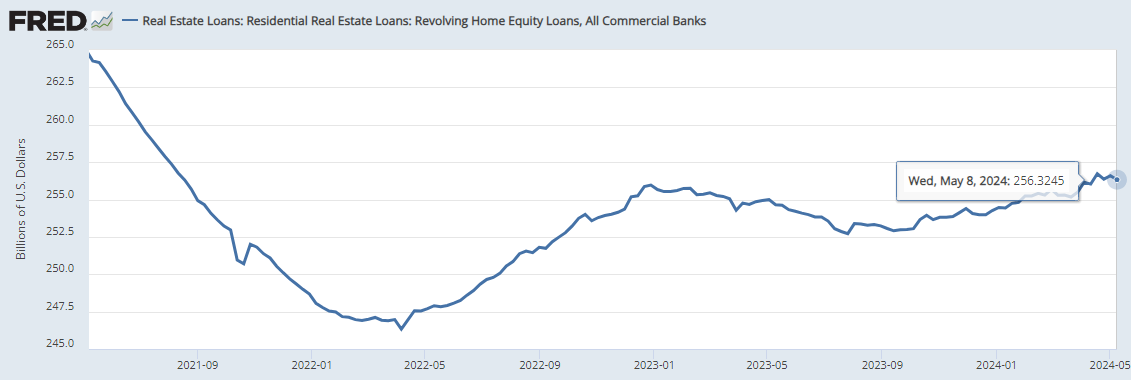

After a steady drop for much of the past decade, Home Equity Line of Credit (HELOC) debt has been ticking up steadily since 2022. According to Experian, the average HELOC balance is about $42,000, up just a bit from $41,000 in 2022 and $39,500 in 2021.

Motor vehicle loans balances actually did not drop during the pandemic, but have similarly surged in the time since, topping out at over $1.5 trillion, which is more than double the debt load on auto loans from the late 2000’s.

Housing

The high cost of homes and rents are a common topic in this newsletter, so I won’t further dwell on them too much here, other than to say the overall housing situation is a big driver in the negative economic sentiment out there. Shelter inflation, which includes both homes and rents, was up 5.5% for the last 12-month period ending in April, outpacing the overall inflation rate once again. Not only does this stretch people’s budgets, which is of course very tangible, it also contributes to the general sense of frustration out there that so many are feeling. As I wrote about last year, many would-be homebuyers have simply given up. Faced with a general sense of futility at buying a home, of course people are going to feel pessimistic about the economy, which is showing up in the polling.

Despite the pessimism out there, missed or past due payments on loans and credit cards are pretty close to historical lows, believe it or not. Home loans, in particular, are showing a low delinquency rate of just 1.69% (although the most recent quarter for which data is available is the fourth quarter of 2023, and I suspect data for the first two quarters of 2024 will show slight upticks). Analyzing home loan data is tricky (and will remain that way for many years) because the pre-2022 home mortgage market looks much different than the post-2022 market. I would speculate that of the 1.69% home loan delinquency rate, a very large portion of those delinquencies are for more recent home loans, which were typically for more expensive homes at a much higher interest rate (a bad combination, mathematically speaking).

Delinquency rates on credit cards and auto loans are more a bit more prevalent, although this is always the case; when people are struggling financially, they will typically make their home payments first and go past due on consumer debt like credit cards and cars as the stakes of these delinquencies are not as high as with a home. According to the New York Fed, nearly 9% of credit cards and 8% of auto loans are delinquent right now, flashing a warning by saying:

For all debt outside of student loans, delinquency has been steadily rising since the fourth quarter of 2021 after historic lows during the COVID-19 pandemic. Credit card delinquencies, in particular, have risen past pre-pandemic levels.

Fed economists further note that credit card delinquencies are most common among maxed-out borrowers, saying:

While borrowers who were current on all their cards in the first quarter of 2024 had a median utilization rate of 13 percent in the previous quarter, those who became newly delinquent had a median rate of 90 percent. This makes sense, since using practically all of your available credit could indicate a tight cash-flow situation. Indeed, credit utilization is a key input in credit scores, which are intended to measure the probability of future default.

What Does it All Mean

There are some positives out there in the economy, for sure, and not just that the stock market is doing well. Existing homeowners have a lot of equity in their homes, for example, thanks in large part to rising home values. This may be one of the primary reasons why HELOC balances are up: people have a lot of equity to borrow against. And it should also be noted that with rising inflation including just the usual appreciation in prices with the passage of time, credit card and auto loan balances are going to rise, too, as consumer debt is just going to be higher on a pure dollar scale as prices rise.

The thread that holds the economy together right now is that people are working. And although wage growth has moderated a bit in recent months, is has still been positive on a year-over-year basis for the past few years. If that thread is cut, however, the economy would be in real peril. If people start to be laid off, or if businesses stop hiring in general, the economy will face immediate problems. Without steady incomes, people would first and foremost not have the money they need to pay for the basic things of living, but people will also start defaulting on debt, which as we saw during the Great Recession can pretty quickly have a contagion effect throughout the rest of the economy as loans go bad.

Lastly, the sour economic mood has another major implication, as well: the impact on the presidential election. Presidents have a harder time getting re-elected if voters are angry, upset, or generally disenthralled with the economy. More on that…next week!

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

Weekly Round-Up

I happened upon an interesting podcast series this week called Acquired. The co-hosts tell stories in 2-3+ hour deep dives about the founding of various companies. This past week during some long hours in the car I listened to an episode about Walmart and the episode about Amazon. I am hooked.

The Prism Substack newsletter had an interesting piece called 30 Useful Concepts. I’ve read it several times over the past couple of weeks. One thing that stood out to me: Prospect Theory:

People don’t weigh gains and losses evenly. We hate losing money about twice as much as we like gaining it. So, for instance, we’d need to gain $20 to assuage the pain of losing $10. This bias toward loss aversion is one of the foundations of economic behavior.

Albert Einstein once wrote a 17-word note on the secret to happiness. What did he say? “A calm and modest life brings more happiness than the pursuit of success combined with constant restlessness.” Words to ponder in an increasingly fast-paced world. The written note itself sold for $1.8 million in 2017. Read more here via The Hill.

Have a great week, everybody!

https://www.marketplace.org/2024/05/17/when-assessing-inflation-its-not-just-the-data-its-also-the-narrative/

Another perspective from the CBO that is a hard sell. It's seems a 10% cost increase will supersede a larger increase in purchasing power.

Another well written piece that skillfully connects relevant factors. My only two thoughts are to share that I'm old enough to remember the interest rates of the mid and late 70's, and to say that re the presidential race I hope readers acknowledge that one of the two old guys competing for the job in no way represents anything traditional; so I am uncertain about the actual effects these things will have on the race.